Buying a home for the first time can be an exciting venture, but it can feel overwhelming if you don’t know where to start. We’re here to help make your experience feel less stressful with our first-time home buyer guide.

In our guide, we’ve broken down the information you should know into steps you need to take as you buy a home. We start with making the decision to buy a home and guide you through the journey up to the point where you close on the property and plan your move.

This guide can act as the starting point before your journey as a first-time buyer but don’t rely on it alone. If you want professional advice from a mortgage broker, reach out for a free consultation.

Making The Decision To Buy

If you’re debating whether you should rent or buy, you’re not alone. There are many factors to consider when deciding to become a homeowner with various pros and cons. Here are some of the things to think about with buying and renting.

Renting

One of the biggest advantages of renting is its flexibility. If you do not know how long you will stay in a certain area, renting can be a practical decision. When you need to move, you can simply let your landlord know and find a new place once your lease ends. Most places only require at least a 30-day notice before you plan to move out.

However, your landlord may also practice their own flexibility and may increase your rent or force you to find a new place. Owning your own home may be more costly and a longer process, but you do not have to answer to a landlord.

Financially, renting does not allow you to build up equity. Many see renting as pouring your money down the drain or paying off someone else’s mortgage, but that’s not always the case. There are a lot of unrecoverable costs associated with owning a home. To learn more about the rent vs. buy decision check out this video from Khan Academy.

Buying

As mentioned above, buying a home means you have the freedom to stay at your property for as long as you want without restrictions on how to decorate your home. However, investing in a home does cost more and you need to make mortgage payments and pay property taxes, unlike a renter. In the event of any issues with home maintenance or repair, you do not have someone to rely on but need to make the fixes yourself or find a professional service.

Because there are a lot of costs associated with buying and selling property, it can take you a handful of years to break even. As a result, you should consider it a long term investment and plan to hold your property for at least 10 years.

One of the most reliable and valuable investments you can make is real estate. Because unlike other investments, a home has utility. You can live in your property, even if the market turns downward. It also acts as a strong hedge against inflation. So when prices everywhere rise, so does your home value.

The government also offers tax incentives to homeowners because it sees owning a home as a good thing. You can receive various available tax credits and avoid paying taxes on capital gains when you sell your property, unlike many other investments. Overall, owning a home is one of the most reliable investments you can make.

Step 1: Check Your Credit

If you want to become a homeowner and have decided that is the best decision for you, you will need to be eligible for a mortgage. The quickest way lenders can see if you can pay back debts before they fund your real estate goals is by checking your credit score.

It may not be the only thing lenders look at when they consider your application for a mortgage, but a good credit score is crucial to receiving the mortgage you need to finance your dream home. Improving your score will take time, which is why it is the first step you need to take before you buy a property.

Apply for A Credit Report

Credit scores are 3-digit numbers between 300 and 900, which are assigned by TransUnion and Equifax, two Canadian credit bureaus. As you may know, a higher credit score is always better than a lower one.

Your credit score tells of your reliability as a borrower. A higher credit score shows mortgage lenders that you consistently pay back debts on time, while a lower score may suggest to lenders that you cannot make regular repayments.

Lenders consider a credit score of 680 to be good at the least, but you want to try to have a score of at least 700. The number fluctuates depending on your spending behaviour on a daily basis, and you want to avoid suddenly becoming ineligible for a mortgage because of a temporary dip in your score.

You can view your score online once a year with no fee at either www.transunion.ca or www.equifax.ca. But keep in mind lenders use a different score when deciding your credit worthiness, so you can’t rely entirely on the free consumer report. When you’re ready to apply for a mortgage, you’ll need to contact a mortgage broker so they can check the real FICO score.

Look for Any Major Issues

If your credit score is lower than you expected, it may help you to ask for a full report. This way you can see where the problems are and change your spending habits accordingly to improve your score before applying for a mortgage and purchasing a home.

Credit bureaus do not share exactly how credit scores are calculated, but five crucial factors impact your score. Keep these in mind as you look at your full credit report.

Payment History

Steady payment history shows lenders that you are consistent and reliable. It is the biggest factor and impacts your credit score the most.

Any partial or late repayments to any debts, including loans and bills, will be counted against you. If your debts were ever sent to collections or written off or you filed for bankruptcy, your credit score will be greatly impacted negatively. The easiest way to improve your payment history is to pay all of your credit cards, bills, and loans on time.

Credit History Length

The longer you have had your credit card, the more responsible you seem. You want to show lenders you can use credit well, and having a credit account open for at least 10 years is more viable to lenders than someone who just opened a credit card a month ago.

The number of years you’ve had your credit account open matters, so it’s good to keep credit cards open for as long as possible after applying for them. You will lower your score by cancelling any cards, so make sure not to cancel them unless you need to.

Available Credit

Your available credit is the second most important factor to your credit score after your payment history. It is not your total credit limit, which shows how much money you can borrow in total, but the amount you can borrow at the present moment.

You can calculate your available credit by subtracting any balances from your current credit limit. For example, you can have two cards with a credit limit adding up to $10,000 overall. If you make purchases of $1,500 on one card and $2,000 on the other, you are using 35% of your limit, which your score will reflect.

You want to use less than 35% of the credit you have available so credit bureaus and lenders will see you as a responsible borrower. Even though it may seem responsible, having lower credit limits will hurt your score more than help.

You want to prove that you are responsible enough to have high credit limits, don’t borrow very much, and can pay it off in a timely fashion.

Credit Inquiries

Credit inquiries, or the number of requests made to get your credit information, are another factor that influences your score.

There are two credit inquiry types: soft and hard hits. An example of a soft hit is requesting a copy of your credit report. Your credit score is not impacted by soft hits. Hard hits are when you apply for credit, like a mortgage, and do affect your credit score.

Lenders may become nervous if you have too many hard-hit inquiries in a short amount of time, and your credit score can go down as a result. This will affect your ability to apply for credit in the future.

Variety of Credit Types

Having various types of credit shows lenders that you can prioritize and manage different types of debt. It also shows that you can most likely handle a mortgage in addition to your other bills and expenses. As a rule, you need ‘2 trade lines for 2 years’ as a minimum. A trade line is any form of debt, like personal loans and credit cards.

Installment loans like car and student loans do count toward your total trade lines, but they also reduce your buying power. And when you pay them off, they go away and don’t count as a trade line. So I generally recommend having a credit card and a line of credit, or two credit cards. Use them every month, and pay them off during the interest free grace period.

Improve Your Habits

If you want to improve your credit score, you will need to change some of your borrowing habits. Here are a few ways you can get started before applying for a mortgage:

- Fully repay any outstanding debt.

- Pay off bills on time and in full.

- Broaden your types of credit.

- Keep old credit accounts and cards open.

- Limit your amount of credit inquiries.

- Have at least 65% of available credit.

Address Any Inaccuracies

If your credit score report has any inaccuracies, you need to address them right away. You can file a dispute with TransUnion or Equifax to correct your information. To make sure it really is an inaccuracy, take a look at your credit reports from both bureaus. The information they provide may be somewhat different.

Some of the common mistakes are including another person’s information on your report, incomplete history of payments, debts you have already paid off in full, and debts that are not yours. These seemingly simple mistakes can have a big impact on your ability to obtain a mortgage.

TransUnion and Equifax have different ways of resolving disputes. Usually, you will submit a document with your written statement indicating which item you do not agree with on your report. If they do not correct the inaccuracy or you are not satisfied with their solution, you can explain more in-depth why you do not agree in a special note.

Need help with dispute resolution? As a mortgage broker I have access to a special support desk with Equifax, so I can help you expedite the correction process. Just reach out.

Step 2: Assess Your Financial Readiness

As a first-time buyer, it’s crucial to be aware of how much you can afford and borrow when looking at properties. After assessing your credit, you can look at how much you can spend. This will give you a more realistic idea of the type of house you can afford, making the process of shopping for a home a little easier.

Lenders use four main factors to assess mortgage applications, which you can also use to determine your finances.

1. Your Income

The amount of income you bring in usually coincides with how much you can spend on a house: the more you make, the more you can afford. Generally, it’s wise to purchase a home that is worth about three times more than the annual income of your household before tax.

If you don’t have a significant other, it will be easier for you to buy a home with another person, like a parent, sibling, or friend. Your combined income will make it more affordable to buy a house especially in places like Vancouver and Toronto where the average housing market prices are much more than triple the average income.

The stability of your income is also important to lenders. Lenders will prefer you to be employed by a reliable company or organization rather than being self-employed or working in a temporary position. Moving between jobs every six months also reflects poorly on you to the lender, and it may not be an optimal time for you to purchase a home.

If you are worried about your job history and income stability, talk to a mortgage broker who can help you find a suitable lender.

2. Down Payment Amount

Like your income, higher is better. Putting down a bigger down payment makes you much more appealing for a mortgage. The minimum payment for a home in Canada is 5% of the property’s buying price. Houses that cost more than $500,000 require a down payment of 10%.

Though 5% is the minimum amount required, it’s always best to pay more. You can become eligible for a conventional mortgage if you put down at least 20% of the purchase price. Lenders generally see you as less of a risk when you pay more upfront, and you don’t have to pay the mortgage default insurance. The insurance is added when you put less than 20% down, which increases your monthly mortgage payments.

Larger down payments also act as a buffer if the housing market falls. Home prices are not always guaranteed to rise, and a larger down payment can protect you from losing money in an economic crisis.

Once you know how much you need to buy a home, examine how much money you are saving each month to determine when you can buy. You may need to adjust your spending habits and budgets to purchase a home as soon as possible.

3. Your Credit Score

As mentioned above, lenders look at your credit report to get a full picture of your spending record. A high credit score will earn you the prime mortgage rate and allow you to add other features that you want.

A lower credit score will give you a higher mortgage rate, which means you will need to pay back more each month. You may also be approved for a small mortgage amount because lenders do not believe you will make consistent and timely repayments.

4. Your Debt Service Ratios

Debt and how you manage various types of debt is the last big consideration. Lenders want to know if you will be able to handle mortgage payments on top of your other bills and debts. To assess your ability, lenders determine two debt service ratios types: Gross Debt Service Ratio and Total Debt Service Ratio.

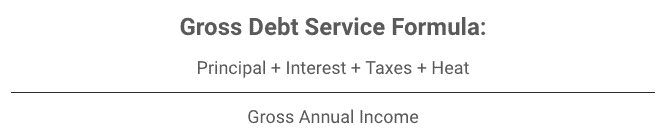

Gross Debt Service Ratio (GDS)

Lenders use the GDS to evaluate how much income you will need to pay for your new house.

- Your GDS can be up to 39% of your annual gross income.

- Your mortgage payment (i.e., Principal & Interest) is calculated at the qualifying rate. At the time of writing, it’s the greater of 5.25% or the contract rate + 2%.

- For help calculating your GDS, reach out to me.

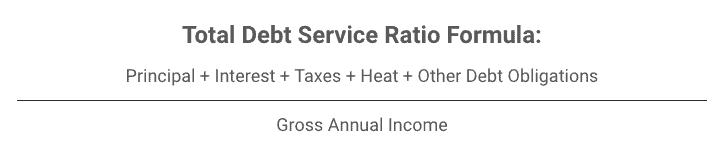

Total Debt Service Ratio (TDS)

While the GDS only looks at housing costs, the TDS ratio is your GDS + all of your debts, including student loan payments, outstanding car loans, or credit cards.

- Your TDS can be up to 44% of your gross household income.

- Depending on your income and debt load, a monthly payment of $300 or a credit card balance of $10,000 can reduce your borrowing power by about $50,000 (or more).

The B-20 Mortgage Stress Test

As housing prices in urban areas rose, the Canadian government decided to limit how much a homebuyer could borrow to pay for their property. Through the B-20 Mortgage Stress Test introduced on January 1, 2018, they wanted to see if buyers could still make regular payments with higher interest rates.

This financial assessment determines if you could afford your home if your mortgage interest rate increased. You must show through the test that you can make the mortgage payments at the current interest rate and the greater of two alternatives: your contractual rate with an added 2% or the five-year benchmark rate of The Bank of Canada, which is usually between 4-5%. At the time of writing it’s 5.25%.

As an example, if you apply for a mortgage that has an interest rate of 2.94%, you need to prove that you can still make repayments on the same house with an interest rate of 5.25%. A higher rate can add hundreds of dollars to your monthly payments. If the added costs put you over the maximum debt service ratios, then you cannot get approved for a mortgage.

Ways You Can Improve Your Buying Power

You may not seem to have enough buying power right now, but there are ways that you can improve it over time as you prepare to purchase a home.

The Home Buyers’ Plan

The Home Buyers’ Plan (HBP) was created by the Federal government to allow Canadians to go from renting to owning a home. If you are a first-time homebuyer in this program, you can withdraw a max of $25,000 from your registered retirement savings plan (RRSP) to make a down payment. If you buy with someone else, that’s a total of $50,000 that you can put towards your down payment.

Your RRSP money is tax-deferred, meaning you do not pay income tax on what you accrue until you withdraw it during retirement. The idea is you will be in a lower tax bracket and won’t need to pay back as much. With the HBP program, you can take out some of those funds to put towards your home with no penalty or tax.

If the HBP seems like the right way to go for you, there are several things you should remember:

- It’s crucial that you fill out the right forms. If you don’t take the funds out with the specific purpose of putting it towards your home or withdraw money that has not been in your RRSP for over 90 days, you will need to pay taxes on your transaction and you will lose your RRSP contribution room.

- You must pay back the amount you take out from your RRSP. You must follow the repayment rules strictly to make sure you don’t end up needing to pay taxes on it. You need to start paying back the amount you borrowed after the first year you took out the funds, and it must be fully repaid within 15 years.

- After borrowing money from your RRSP, it’s a smart idea to make low-risk investments within your retirement savings plan. You want to avoid losing a lot of your down payment when you are saving to buy your first house.

Use Gifted Money for Down Payments

With soaring housing prices and tighter mortgage regulations, a gifted down payment from parents or grandparents has become more popular over the years.

Gifted money is not expected to be paid back and typically needs to come from a close, or immediate, relative. Some buyers use gifted money to pay the full down payments of their first home, while others use it to avoid CMHC fees and meet the 20% requirement. Check to see if your lender has certain rules about gifted money, as they need to know from where your money comes.

However, though your down payment may be covered, you will still be required to show that you can afford all continuing costs of buying a home.

Even if your parents cannot afford to contribute to your home, they can act as a guarantor or co-applicant for your mortgage application to increase your chances of approval.

Buy with Friends or Family

Getting into real estate is much easier when you do it with friends or family. You buy a house with someone else to make it more affordable even if only one person decides to live in it. No matter what kind of relationship you may have, it’s important to keep it professional when it comes to buying a property together.

Ask a trustworthy real estate lawyer to write a detailed agreement for your arrangement, which includes an escape clause in case one party faces financial difficulties or wants to sell the home.

Create a Flexible Budget

After determining how much you need to afford a down payment and continuous costs on your home, test your finances on your own. As a first-time buyer, you do not want to stress yourself out with overwhelming additional payments alongside the bills you already pay if your finances will be stretched too thinly.

The debt service ratios may assess your eligibility for a mortgage, but it does not factor in other daily costs like transportation or childcare. They also do not look at the amount you pay for taxes, EI, and CPP, which all come out of your gross income before you can put it in the bank.

Here are some stress tests that you can use to assess your finances on your own.

Interest Rate

You can use a host of online calculators to determine your potential mortgage payments as you save up for a house. This can help you expect how much you need to save to afford a home as a first-time homeowner.

However, in calculating, use the hypothetical high-interest rate, which is about 2% higher than average, instead of the posted rate. This way you will definitely pass the mortgage stress test and have extra in the case of unforeseen costs.

Cash Flow

Calculate your usual monthly expenses and income after taxes. Then add all the costs you can think of related to owning a home, including property taxes, mortgage payments, using the higher interest rate, costs for maintenance and repair, home insurance, renovations and upgrades, decorations, and furnishings.

Have a realistic expectation for the amount of money you want to have left for other things, like emergency savings, vacations, dining out, and entertainment.

Life Events

After calculating your cash flow, test it using various probable scenarios. For example, what do you do if you lose your job? What if you decide to take classes or go back to school? What if you have children or buy a car?

In these different scenarios, would you still be able to make the necessary payments and also afford additional housing costs? Due to the volatility of life, it is vital to be financially prepared for any unforeseen event.

Having a buffer of affordability is crucial in deciding what kind of home you can afford. You don’t want to find yourself struggling to make payments if interest rates go up or you face additional or emergency expenses.

A good mortgage broker and financial advisor can help you decide on the appropriate buffer for you and provide essential guidelines. A financial professional can also help you come up with a detailed strategy to save up to afford the home you want to own.

Here are some general tips to get you started on preparing your finances:

- Avoid new debts and pay off debts with high interest.

- Try not to make major hard-hitting purchases on your credit cards that will significantly impact your debt ratios.

- Seek reliable and stable employment if you are currently in a part-time or temporary position.

- Set savings goals for each month and adjust your budget accordingly.

- Make sure you have enough funds in your RRSP if you decide to utilize the Home Buyers’ Plan.

- If your dream home is unaffordable after conducting the tests, consider a different housing type or location and a lower target price. Then try the stress tests again.

Step 3: Receive a Pre-Approved Mortgage

Mortgage professionals can give you more information on the type of home loan you should expect. There are two options you can go to for guidance: a mortgage broker or a bank.

Mortgage Brokers

A mortgage broker is an excellent option if you are shopping around for the lowest rates. Brokers save you money and time by searching the market for you to find the best mortgage that fits your requirements and comes at a low rate.

They are not associated with a single lender and can view rates that are not visible to those outside the industry. Even if you visited the same lender directly, mortgage brokers can get you a lower rate because of their knowledge and expertise. Not all lenders work with brokers directly, but your mortgage broker can tell you whom they do not work with while still having access to the rest of the mortgage market.

You can also avoid any hard hits to your credit with a mortgage broker because brokers talk to several institutions and lenders for you. They are more flexible and can often communicate with you remotely, making the pre-approval process much easier for many first-time homebuyers.

The best part is that most mortgage brokers don’t cost a thing. They are most often compensated directly by your lender after approving your mortgage.

Banks

Banking institutions can be a comfortable option since most people have a trusted relationship with at least one. Making new decisions as a first-time homebuyer can feel less overwhelming when you deal with representatives from your bank. Banks might even offer some perks, like waiving home appraisal fees.

However, there are some downsides to working with a bank. Unlike a mortgage broker that presents all available options, a bank representative only recommends the rates and products their institution offers. You will need to reach out individually to several institutions to shop for a lower mortgage rate, which can be time-consuming and damaging to your credit score.

Your bank will most likely not offer you the lowest interest rate in the beginning, requiring you to negotiate until you get it down to what you want.

Pre-Approved vs. Pre-Qualified

Even if you haven’t decided if you want to purchase a home yet, getting pre-approved or pre-qualified for a mortgage gives you an idea of the amount of money your lender will allow you to borrow.

Getting pre-qualified is an easy way to calculate costs for those still on the fence about buying a home. You input basic information including your down payment amount, a summary of debt, and income, and then you receive a mortgage estimate. However, it is only an online estimate. Your lender will need to do a credit check and verify your information before you can get a concrete idea.

If you are fairly certain you are ready to purchase your first home, you can skip to the pre-approval. You will need to provide some documents in addition to your income and debt summaries, including:

- Government-issued ID, like a driver’s license

- Letter of employment confirming position, tenure and income (within 30 days)

- Recent pay stub (within 30 days)

- Notice of Assessment (2 most recent years)

- T4 Slip (2 most recent years)

- Proof of down payment (90 days of bank statements)

- List of assets

- A gift letter (if applicable)

The mortgage broker will also ask for your permission to look at your credit report and credit score. After your offer on a home has been accepted, they will review it all again to ensure everything is in order. At this point, you will be able to settle your mortgage with the interest rate and loan conditions.

After receiving a pre-approval for a mortgage, you can hold onto the calculated interest rate for up to 120 days. If you apply for a mortgage within that time, you will receive the quoted interest rate even if rates have increased.

Once you’ve got your mortgage pre-approved, you can finally start searching for a house with an informed and realistic idea of the price you can afford.

Though it may seem like a sure deal, a pre-approval does not guarantee a mortgage. It also requires lenders to inquire about your credit score, which is a hard hit. Avoid sending in multiple applications because it can damage your credit. Find a mortgage broker who can assist you in attaining pre-approval without impacting your credit score.

In addition, a pre-approval doesn’t always mean you can afford the maximum mortgage amount quoted to you. Make sure you review all of the factors that could impact your finances before you begin house hunting.

Common Mistakes to Avoid

Before purchasing your first home, there are a few common pitfalls you want to avoid.

Neglecting the Canadian Mortgage and Housing Corporation Fee

A high-ratio mortgage is classified as such when the down payment falls below 20%. You will then be required to purchase mortgage default insurance, which is added to your mortgage, from the Canadian Mortgage and Housing Corporation (CMHC). This extra fee is designed to protect the mortgage lender if you fail to pay back your mortgage.

The CMHC fees are tiered according to the down payment percentage. For example, someone with 10% down will pay a higher amount than someone with a 15% down payment for the same-priced property.

Not Preparing for Closing Costs

Settling a mortgage requires cash, and you don’t want to take it out of your down payments funds or be caught without it. It’s crucial to estimate beforehand how much you will need to pay the closing costs on your mortgage.

Exceeding the Revolving Debt Amount

Revolving debt is the balance on your credit line. It is not unusual to carry debt on credit cards, for example. However, before you apply for a mortgage pre-approval, focus on paying off credit card debts so you can keep your credit utilization under 50%.

For example, if you have a credit limit of $10,000, you should not exceed a total balance of $5,000 on your credit cards. Lowering your credit limit will not help your credit score; rather, it will negatively impact you by lowering the 50% threshold. If you find yourself going over the threshold, you should consider increasing your limit.

Step 4: Deciding on the Mortgage Type

Choosing the right lender, interest rate, and type of mortgage for you is crucial since you will most likely be paying off your house for a long time. If you don’t go through the process carefully, you may end up losing hundreds or thousands of dollars in future savings.

After receiving pre-approval for your mortgage, there are several questions you should ask your lender or mortgage broker. Deciding on what mortgage type works for you and how long you want to make repayments will save you time and allow you to create more accurate budgets while looking for a home.

Mortgage Types

The first and most arguably most important question is the type of mortgage interest rate you get. There are two types of interest options: fixed-rate and variable-rate.

Fixed-Rate

With a fixed-rate mortgage, you will know how much interest you can expect each month on your loan. Its predictability makes budgeting easier and allows you to set aside the same amount each month for the whole mortgage term. It can also safeguard you if rates increase substantially in the future.

A fixed mortgage (typically) comes with a higher rate than a variable mortgage. You can see this higher rate as a a ‘safety premium’ because it guarantees your rate won’t fluctuate.

Homeowners typically decide on this option so they know what to expect and don’t have to worry about their rates adjusting each year. If you ever need to break your mortgage, a fixed rate has higher penalties than a variable one.

Variable-Rate

Variable-rate mortgages are pegged to the bank’s prime rate. So for example if the prime rate is 2.45%, you might get a rate of Prime – 0.50%, which is 1.95%. It can go the other way, too. Typically for home equity lines of credit, your rate could be Prime + 0.50. Which in the above case would be 2.95%.

If the prime rate increases, more of your payment will go toward interest rather than the principal, increasing your interest and the time it will take to pay your mortgage in full.

However, if the prime rate decreases, your money will pay off more of the principal, lessening the time needed to fully pay off your mortgage without you making additional payments. If you believe mortgage rates will fall or remain the same, it makes the most sense to choose a variable-rate mortgage.

Pre-Payment Options

Mortgage prepayments are extra funds that you pay towards your home on top of what is required during each pay period.

Unlike a regular mortgage payment which goes towards the principal and interest, all of the extra funds go directly to paying off your principal balance. Making prepayments helps you speed up the process of fully paying off your mortgage and saves you thousands of dollars in interest.

There are a few benefits to making prepayments. Mortgage penalties decrease the more prepayments you make. It also shortens your amortization period or the amount of time you are scheduled to repay the loan. You will also have more flexibility to lower your regular monthly payments if you need to.

Lenders usually allow you to increase your monthly payments, pay lump sums when you can, and schedule extra mortgage payments. For lump sums, there are limits to how much you can pay at one time, which typically falls between 10% to 20%. They may also have limits on how often and when you can send in prepayments.

Making prepayments is a great way to pay your mortgage in full earlier than scheduled, but you should pay off other high-interest debt first, such as credit cards. You can ask your lender or broker about more prepayment options if that is something you are interested in.

Frequency of Payments

How frequently you make your payments will affect how quickly you can pay off your mortgage and the total amount of interest. Here are the most common options for frequency and how to calculate the amount of each payment:

- Monthly

- Semi-Monthly (monthly payment ÷ 2)

- Biweekly (monthly payment x 12 ÷ 26)

- Weekly (monthly payment x 12 ÷ 52)

- Accelerated Biweekly (monthly payment ÷ 2)

- Accelerated Weekly (monthly payment ÷ 4)

Through accelerated payments, you make one extra monthly payment every year, saving you thousands of dollars on interest costs over your mortgage’s lifespan.

Many buyers choose a frequency that aligns with their scheduled payday. For example, one may choose to make payments biweekly because they get paid biweekly.

Cost of Penalties

When you apply for a mortgage, you most likely don’t think about breaking it. Most Canadian homeowners prefer a five-year fixed-rate mortgage according to mortgage lending data, but more than half of them end up breaking them before their term ends.

This could happen for several reasons. You could lose your job, become ill or need to pay emergency medical bills for someone else, sell your home before your mortgage term finishes, or change lenders. Typically, breaking your mortgage comes with a significant penalty. Before signing up for your mortgage, it’s a good idea to be aware of how much that penalty is to avoid any surprises later on.

Your mortgage type dictates the penalty amount. Variable-rate mortgages have a standard fee of three months of interest. A fixed-rate mortgage usually has a higher penalty fee: you pay either three months of interest or the Interest Rate Differential (IRD), whichever is the greater amount.

Lenders calculate the Interest Rate Differential using a complicated formula and current market interest rates. If you have a fixed-rate mortgage, find out if your lender uses the pricier posted rate or the more economical discounted rate in calculating the penalty fee.

Mortgage Portability

When you change lenders or move houses before the end of your term, having a portable mortgage is extremely beneficial. You get to keep the same interest rate, don’t get charged for early repayments, and are not required to pay penalty fees.

Fixed-rate mortgages are often portable while variable-rate ones are not. Talk to your lender beforehand to learn what restrictions there are to portability. You will usually have a set number of days to close your old mortgage and set up your new one to maintain the same interest rate and other conditions. The timeline varies from 30 to 120 days.

Though you may get to transfer the same interest rate and other conditions to a new mortgage, you still need to go through the loan application process. That means you’ll need to show the required documents and complete the same steps as before to prove your financial capability.

If you end up taking on a bigger loan with your new mortgage, you can usually blend your mortgage depending on your lender. A blended mortgage means lenders will find some kind of compromise between the conditions and rates of your old mortgage and the conditions of the new one.

Step 6: Search for a Home

Now that you have a solid idea of the type of home and mortgage you can afford without worry, it’s time to start looking for a house. There are a few ways you can get started with this, such as enlisting help like real estate agents.

Make A List of What You Want

When purchasing a home, you want to invest in a property you will keep and live in for five years at least. Before you start shopping around, make a list of the things you are looking for in a home. This can be split into two different sections: the required features you won’t compromise on, such as the property type or neighbourhood, and features that would be nice but are not required, such as a pool or patio.

Required Wants

Creating a list of the things you absolutely need in a home will help a realtor narrow down your choices and present you with homes that fit most closely with your needs. It can make the search much more manageable with fewer options to choose from. Here are some of the requirements that you may want to consider putting on your list.

Location

Location is key when it comes to buying a property. Decide how far you are willing to relocate and if the commute to work, family, and friends are doable. Choose the most sensible areas with your partner or loved one that is within the proximity you want.

You may want a home closer to work if traffic will be a problem, a house closer to family and friends, or a property in a quieter suburban area near good school districts.

Neighbourhood

After deciding on your ideal locations, think about the neighbourhood. What features do you want your potential neighbourhood to have? A great school your kids can walk to? A major hospital nearby if you have any health concerns? Low crime rates and a safe park where kids can play?

When you eventually decide to sell your house, think about how the area around your house will look to potential buyers. If your property is near a highway or railway, those features may be appealing, but they may not appeal to buyers as much when the market is slow. Consider how your home will be impacted by other things in the surrounding area, such as its proximity to grocery stores, restaurants, and parks.

Another important factor to consider is the people who may become your new neighbours. Do you want a home in a neighbourhood with lots of families or single or coupled working professionals? Do you want the area to be lively or quiet?

When you attend an open house, don’t be afraid to chat with some of the neighbours to get a better feel of the area. You may find many people don’t mind answering a few questions to tell you about any significant issues or their experiences living in the neighbourhood.

Housing Type

The best housing type for you depends mainly on the size of your family and your budget. You can go with a house, condo, or townhome, and each one has its pros and cons.

Houses are generally the most expensive out of the three depending on the area. They also require more maintenance and have many additional costs such as utilities, home insurance, and property taxes. However, they come with the most privacy and freedom for you to bring in pets, renovate, or make other changes to the property.

Condos are a great next step from renting as it comes with fewer maintenance responsibilities. The added fees that come with condominiums protect you from large or sudden costs and you have access to appealing amenities. However, you may face strict limitations and rules, unexpected costs for special maintenance, and experience less privacy overall.

A townhome is a combination of a house and a condo. It provides more space and privacy than condos and comes at a lower price compared to a house. Many townhouses come with association fees to maintain the neighbourhood grounds.

Bedrooms & Bathrooms

Almost all residences on the market advertise how many bedrooms and bathrooms the property has. Decide how many rooms you need at a minimum for your family size and if it will be enough for the next several years.

If you plan to start a family, you may want to purchase a home with more than one bedroom. Starting the process of buying a different home in just a few years will only cost you more money in the long run.

Age of the Home

The age of your home may not matter as much if it has been recently renovated or updated in the past several years. When you buy a home that is being resold, you may not always like how the last resident(s) decorated it and they may have neglected some areas of the home. That’s why conducting a professional housing inspection before you commit to buying is crucial.

If you want to make renovations to an older home, add that into your budget and know what repairs and alterations you should expect before making a bid. However, a home that has been lived in previously is usually located in a well-established neighbourhood, near public transit, and close to other conveniences.

Resale houses also provide more flexible mortgage terms and more reliable dates for closing on the property. You also don’t need to pay the Goods and Services Tax/Harmonized Sales Tax (GST/HST) fees, which come with purchasing a newly-built home.

There are several perks to buying a brand new house. For one thing, it is your property and you get to customize every little detail to your liking from the very beginning. However, houses may take a while to build and there may be delays for various reasons. You will need to pay extra costs for landscaping, customized features, and fences.

The home builders may also require you as the buyer to make your down payment in scheduled installments, which may affect your budget and financial plans. There is typically less flexibility when it comes to the buying price and you can’t avoid paying the GST/HST fees.

Nice to Have But Not Required

You may need to be flexible when looking for a home especially if homes in your desired area are not as readily available. After creating your list of required needs, make a list of features you’d like to have but don’t need. It may not be possible to find a property that has every single thing you want, but you can still find properties that have a few features from your not-required list.

You can put virtually anything on this list, but here are some you may want to consider:

- Backyard

- Garage

- Parking

- Type of street

- Proximity to highways or major roads

- Design

- Patio or Deck

- Pool

- Floors

- Basement

- Laundry

- Certain upgrades

Get the Best Professional Help

When you look to buy your first home, it may be confusing and overwhelming at times. Seeking guidance from professionals can be very helpful in broadening your options and helping you with paperwork or other important decisions.

As mentioned earlier, a mortgage broker or major bank is essential when it comes to finding the lender offering the best mortgage rates for your home type. Here are some of the other services you will need or may want on your home-buying journey.

Real Estate Agent

For first-time buyers, enlisting a realtor or real estate agent can make shopping for homes much easier. Real estate agents receive their commission from the seller, which means they typically offer helpful advice virtually for free. An experienced realtor can even show you housing options that are not officially posted yet.

Though not everyone decides to go with an agent, they can offer useful guidance if you have never owned a home before. If you choose to seek a realtor’s help, make sure the one you choose is familiar with your desired neighbourhood and the type of property you want.

There are various ways you can find a reliable real estate agent, such as looking at “For Sale” signs and open houses, asking friends and family, or checking out local brokerages. Make sure you look at all of your options before deciding on the best agent that can meet your needs.

Real Estate Lawyer

When you close on a property, you need to have a real estate lawyer there in the process. Finding a lawyer you can trust and building on that relationship before even looking for a home is crucial so you don’t need to worry about finding one later on. You can find real estate lawyers through referrals from your real estate agent, friends and family, or online searches.

Home Inspector

Once you make an offer on a home, you may want to have a professional inspect the home to make sure everything is in order. You will need to arrange this on your own if your offer is accepted, and real estate agents can most likely refer a couple of local, highly qualified home inspectors. Make sure they check for mould and moisture, which could be detrimental if left unchecked.

Resources for Home Shopping

Now that you know exactly what you are looking for, it’s time to look for the house that fits your budget and provides everything on your list of required items. If you have a real estate agent, you will receive listings that match your preferences. They will also arrange home viewings and keep you informed of what’s on the market as soon as new listings pop up.

You can also keep an eye out on your own to see what properties are becoming available in a number of different ways.

Multiple Listing Services Website (MLS)

Real estate agents use the MLS website to find more specific properties that match your interests. You can browse through it yourself to take a look at some of the options on the market. It’s a great way to get an idea of what is out there without needing to visit every single listing.

‘For Sale’ Signs

Not all properties will be listed on the Multiple Listing Services website, so you may find additional properties by keeping an eye out for houses with lawn signs that read “For Sale.” If you spot a home you like, ask your realtor for more information about the property and stop by an open house or schedule a tour.

Social Media

Nowadays, businesses and organizations post advertisements and information on social media, including real estate. Use Facebook or another social media platform to follow realtors. They may post advertisements for homes on sale, and you might find something within your budget that matches your requirements.

Family & Friends

The people in your network can be a great personal connection when you look for a home. By telling your family, friends, coworkers, and others that you are planning to purchase a property, they might let you know early on if they are thinking of selling their home or know of someone else. This allows you to check out the property and make an offer before others can.

Step 7: Propose an Offer

After finding the place you want to call home, it’s finally time to propose an offer. Make sure to take all the precautions with your offer as you most likely aren’t the only person bidding for the property.

Set the Price

There are several factors you will need to consider when deciding how much to offer on a home. You want to look at the listing price, any potential remodelling, and how much other homes in the area are selling. However, homes are not always priced correctly and they may not sell for the initial asking price. If you have a realtor, they can help you decide on what you should offer.

The housing market also influences the right price. There are three types of markets: sellers, buyers, and balanced. In a seller’s market, those selling a home can pick and choose from a multitude of buyers. Many buyers will compete for a smaller number of houses, making prices inflate. In this situation, offer your best amount first to make sure you stand out from the competition.

In a buyers market, it’s buyers who get to choose from more housing options. This is when there are more homes available than buyers, giving those looking for a home the ability to negotiate, offer a low price, and add more conditions.

A balanced market is where the number of buyers and sellers is about the same. They can both negotiate and decide on a decent price for homes despite the rate of inflation.

Additional Contingencies

Before you fully commit to a home, you want to make sure to protect yourself and your deposit. As you create your offer, you have the choice to add or waive conditions.

Conditions are any needs the buyer wants to ensure are met before committing to the property. Finances, home inspections, and emergency repairs are common examples of contingencies you may want to include. If any issues arise, you can notify the seller of what needs to be changed or you can rescind your offer without consequences. Contingencies can be about almost anything.

For buyers, waiving all conditions is a risk. You may not know the full story of the house until you complete an inspection, and there could be mould or structural issues. You might end up with thousands of dollars of unforeseen repairs after making your offer if you are not careful. However, some buyers do not include conditions in a seller’s market to make their offer more competitive in bidding wars.

For first-time homebuyers, including a financial contingency can be important. It can protect you in case your mortgage request is not approved. It can also act as a safeguard against a home that is not priced accurately.

The home you choose may be valued at more than what you can afford, which is often only discovered after your lender conducts an appraisal. If you cannot afford it, walking away without a condition of financing in place may cause you to lose your deposit and possibly get sued by the seller.

If you have a real estate agent, they can work with you to come up with an offer and then present it to the sellers. If you purchase a brand new home, you propose your offer to the builder, who is the direct seller. There are not usually bidding wars on newly built homes, but there is also less room for negotiations.

The Offer is Approved–Now What?

Once your offer has been approved, congratulations! That’s a huge step, but there’s more to do before you can start calling the house yours. Here are some of the big things that still need to be finished before closing on the property.

Pay the Deposit

Once your offer is accepted, you and the seller will need to sign a contract of sale with a deposit made by you. Unlike a down payment, a deposit is made to show that you are committing to the purchase deal and ensuring the seller won’t offer the property to someone else.

The deposit amount varies between a few hundred to 4-5% of the home price. The money you initially pay will go towards your down payment later on after the deal is closed. The deposit details will be included in the contract, and once you sign you will have to make the payment within 24 hours.

Conduct the Home Inspection

A home inspection is crucial before you buy and can be included as a condition on your offer. Enlist a qualified home inspector, which can be recommended to you by your real estate agent, and schedule the inspection as soon as possible. You want to find out if there are any major issues as soon as possible so the seller can address those without significantly delaying your move-in process.

Secure Your Mortgage

The appraisal your lender requests will confirm if the house price matches its market value. Many lenders will ask you to pay for it, but some may cover the appraisal cost. If you find out that the home is worth more than your initial price, you will need to cover the additional cost.

The lender will also double-check all of your information, such as your income, debt, and credit score to see if your finances have changed at all since your pre-approval. They want to know if you still have enough money to buy the property and can make regular payments as an employed individual.

Avoid making any large purchases on your credit card to ensure your score doesn’t change much before completing the deal. If everything looks good, your lender will approve your mortgage.

Bring in a Real Estate Lawyer

After getting your mortgage approved, a real estate lawyer is essential in closing your deal. They register the home for you under your name, calculate land transfer taxes, make sure the title of the home does not have any liens or defects, creates the statement of adjustments, buys title insurance, prepares paperwork for your mortgage, and lastly hands you your new keys.

You want to make sure you hire someone you can trust with these important documents and the entire process.

Make a Final Walkthrough

Throughout the process of buying your first home, you want to make sure you walk through the property several times. You can show the house to loved ones and get room measurements for furniture pieces. Before you officially move in, conduct a final walkthrough and take a look to see if there are any damages or changes made that may affect your decision to commit.

Schedule Your Move-In Day

The best time to move into your new home is a couple of days after the deal is scheduled to be finalized. That way movers won’t be waiting for you to finish closing the deal and you have some flexibility to pack up final items and furniture.

Step 8: Begin the Closing Process

The last step before you are officially a homeowner is the process of closing the deal. Everything needs to go smoothly. Any missed steps can delay the process and may even prohibit you from owning your new home.

Final Closing Costs

Closing costs are the disbursements and fees which are required to complete a deal. The amount depends on your location, and many first-time buyers receive some leniency on these extra costs.

These amounts are often known as real estate’s hidden costs. Buyers don’t always budget enough to prepare for these closing costs, which are significant amounts of money. These costs cannot be negotiated, so make sure you have enough saved up. Two of the most common costs are real estate lawyer fees and land transfer taxes.

Lawyer Fees

Your real estate lawyer will charge you according to your lender and the deal you need. They can cost thousands of dollars, so make sure you prepare at least two thousand dollars or more to spend on legal fees. Though it may seem more economical to go with a cheap lawyer, having a reputable professional can make a huge difference in how smoothly the closing process goes.

Land Transfer Taxes

Your land transfer taxes is how much you need to pay your province to buy a property. The cost will depend on the location of your house. In a major city like Toronto, you will be required to pay a provincial and municipal tax.

If you buy a home for the first time, you may receive a refund on almost all of what you pay. To get an estimate, you can use an online calculator to figure out how much you should expect to pay on taxes.

Other closing costs include:

- Home inspection

- Appraisal fee

- Title insurance

- CMHC insurance

- Utilities and property tax adjustments

- Utility hookups

Final Step

The average house can take between 30 and 90 days to complete the closing process. The number of days will be included in your offer. Have one last meeting with your lawyer about a week before you close on the property. During this meeting, finalize your deal and make sure to read everything and carefully sign all of the necessary paperwork for your mortgage. This is the last time you can catch any mistakes or make changes to your contract.

To close your real estate deal, send your lawyer the final amount for the down payment using a certified cheque. Your lawyer will call you once they have registered the home under your name, and then you can swing by to pick up your new keys.

Right when you enter your new home, take a look around to make sure there are no other issues. If you notice something amiss, make sure to let your lawyer or the seller know immediately.

If everything looks great and you’ve got the keys to your new house in hand, congratulations! You’re an official owner of your first home!

Conclusion

Becoming a homeowner for the first time is an incredible achievement that takes careful planning, time, and saving.

The crucial first step is making sure you have enough money to cover a house, hidden costs, and other fees that come with it. However, by setting goals, using government programs, and being flexible with what you want in a home, you may be able to buy a house faster than you expected.

Once you own a home, you will most likely remain a homeowner for a long time. With the right lenders and steady income, you can save thousands of dollars, build up your equity, receive tax breaks, and gain value on your home.

Working with experienced and reputable professionals like real estate agents, lawyers, inspectors, and brokers is crucial to making the home buying process go smoothly. It will ease a lot of your stress and even speed up the process. You may even end up with your dream home thanks to their professional expertise.